.webp?width=1200&height=800&name=what-is-a-certified-peo-jo-mcclure-Axcet-HR%20(1).webp)

Understanding the distinction between a CPEO vs PEO—or more precisely, a certified PEO vs. non-certified PEO—is crucial for small and mid-sized businesses (SMBs). These companies make up nearly half of the U.S. workforce and often operate with limited internal HR resources.

Running an SMB means juggling multiple demands—from managing employees and maintaining compliance to staying focused on growth.

Given these demands, outsourcing HR functions can be a game-changer. That’s where professional employer organizations (PEOs) and certified professional employer organizations (CPEOs) come in.

But what’s the difference between a CPEO vs PEO, and why does certification matter? Let’s break it down.

A PEO (Professional Employer Organization) is a firm that provides HR services to businesses through a co-employment relationship. These services typically include:

✔ Payroll processing

✔ Employee benefits administration

✔ HR compliance assistance

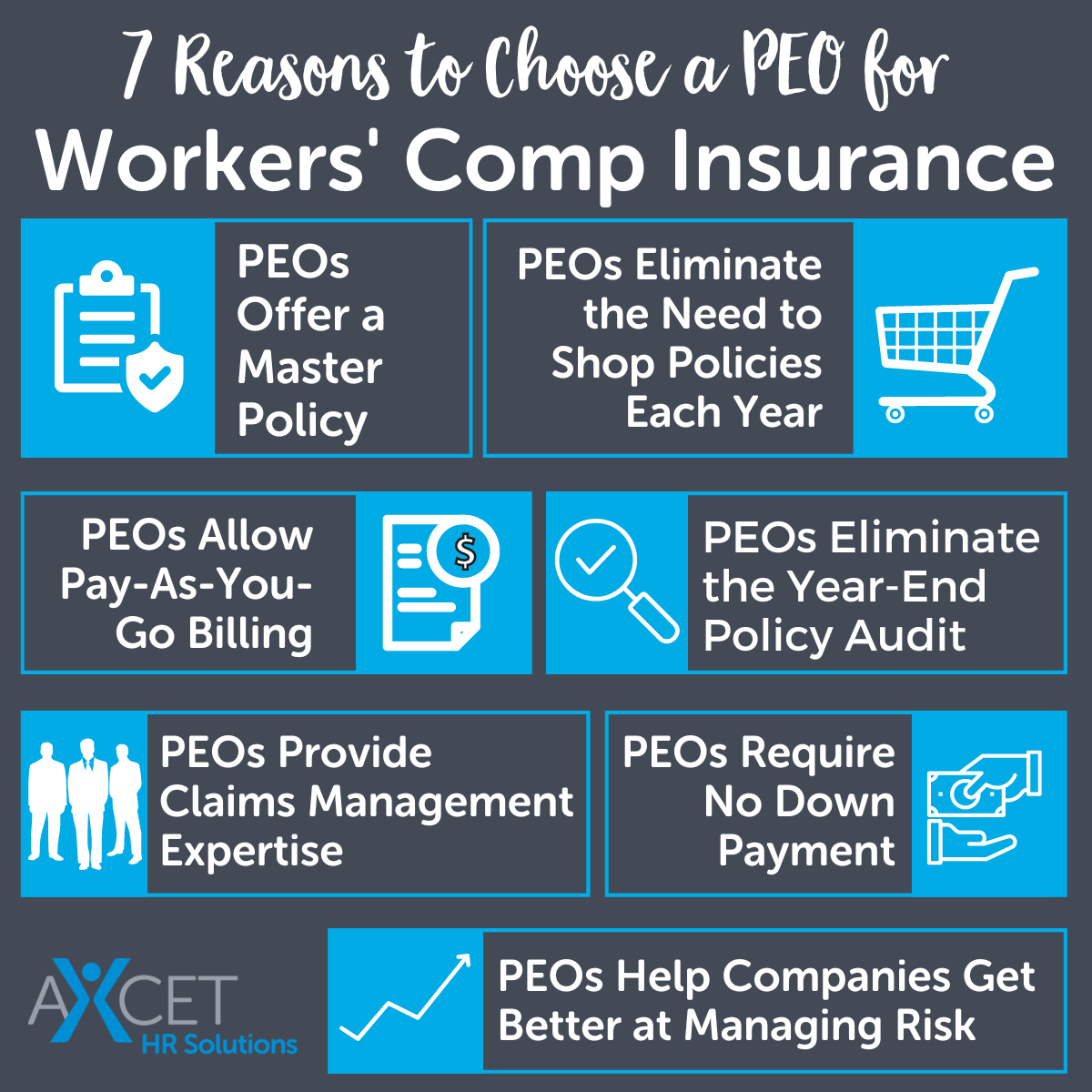

✔ Workers’ compensation and workplace safety

Under this arrangement, the PEO becomes the employer of record for tax and benefits purposes, while the client company maintains day-to-day responsibility for managing employees.

However, a traditional, non-certified PEO does NOT assume sole liability for employment taxes. If the PEO collects payroll taxes but fails to remit them to the IRS, the client company may still be held liable.

A CPEO (Certified Professional Employer Organization) provides the same HR and payroll services as a traditional PEO but with one key distinction: It has successfully met the IRS's strict requirements for certification.

This certification provides important tax advantages to businesses, including:

✅ The ability to retain federal tax credits (which may be lost under a standard PEO).

✅ Elimination of wage base restarts for Social Security and Medicare taxes when switching mid-year.

✅ Sole liability for employment taxes—once the client pays the CPEO, the IRS cannot pursue the client for unpaid payroll taxes.

Additionally, CPEOs must adhere to continuous IRS reporting and bonding requirements, ensuring their financial stability and compliance with federal regulations.

RELATED: The Best PEO Meets These 5 Qualifications >>

Both certified and non-certified PEOs provide HR outsourcing services, but only a certified PEO (CPEO) carries IRS recognition, financial safeguards and specific tax protections.

Understanding the difference between a CPEO vs PEO can impact everything from tax liability to long-term peace of mind.

While the comparison chart above provides a quick comparison, understanding the full impact of these differences can help businesses make a more informed decision.

It's also important to understand how PEO pricing works and what services are included so you can evaluate the overall value of each provider—not just the monthly cost.

Let’s take a deeper look at the five biggest distinctions between a certified PEO vs non-certified PEO.

A CPEO must meet rigorous IRS standards that a non-certified PEO does not. These include:

Traditional, non-certified PEOs do not undergo this level of scrutiny.

With a non-certified PEO, both the PEO and the client share tax liability. If the PEO fails to pay employment taxes, the IRS can pursue the small business for unpaid amounts—even if the business already sent the payments to the PEO.

With a CPEO, the IRS recognizes it as the sole party responsible for tax payments. Once the business pays the CPEO, it is legally protected from any further tax liability.

One major concern for small businesses considering a PEO is whether they will lose access to federal tax credits.

Switching to a traditional PEO mid-year can trigger wage base restarts, meaning businesses may have to pay payroll taxes twice on the same wages due to a change in the Federal Employer Identification Number (FEIN).

A CPEO prevents this issue, allowing wages already paid earlier in the year to continue counting toward annual Social Security and Medicare limits.

A CPEO provides a higher level of financial security, tax compliance and risk mitigation. This added protection is one reason many businesses choose a CPEO vs PEO.

Consider this: Would you choose a bank that isn’t insured by the FDIC? Most business owners wouldn’t. The same principle applies when choosing an HR provider—IRS certification provides important safeguards.

Now that we've covered the main difference between a certified PEO vs non-certified PEO, let's learn more about CPEOs and PEOs, and the services and benefits they provide small to mid-sized businesses.

Not all PEOs are created equal. The biggest distinction between a certified PEO vs non-certified PEO comes down to IRS recognition and the legal protections that come with it.

While both may offer HR services, only certified PEOs can shield clients from federal tax liability and wage base restarts.

The IRS created the Certified Professional Employer Organization (CPEO) program to increase accountability and transparency in the PEO industry.

Because of this, the certification process is rigorous. The IRS sets strict requirements that must be met before certification is granted. To qualify, a PEO must:

✅ Undergo a rigorous IRS review process, including financial audits and tax compliance checks.

✅ Provide extensive documentation proving it has paid all employment taxes on time.

✅ Maintain positive working capital to demonstrate financial stability.

✅ Ensure that all key personnel pass background checks, particularly those responsible for tax payments.

✅ Submit quarterly CPA-reviewed tax filings to confirm ongoing compliance.

✅ Post a substantial IRS-mandated bond to guarantee its ability to meet payroll tax obligations.

Only a small percentage of PEOs achieve CPEO status. In fact, among the hundreds of PEOs operating in the U.S., fewer than 10% have achieved IRS certification.

RELATED: Why Use a PEO Instead of an HR Person >>

Axcet HR Solutions is proud to have met the IRS’s rigorous certification requirements, including a documented history of federal, state and local tax compliance, financial responsibility and organizational integrity.

We were among the first 10% of PEOs nationwide to achieve IRS certification, and we have maintained that certification uninterrupted since first earning it in 2017.

In fact, we are the only local PEO headquartered in Kansas City to have received the IRS designation of certified PEO and to have maintained our certification, uninterrupted, since first earning it in 2017.

“Axcet HR Solutions is committed to operating according to the highest standards. We take every measure to ensure our clients have the utmost peace of mind when they partner with us for all of their business’ HR needs.”

-Jo McClure, Axcet HR Solutions Director of Payroll Administration

Both CPEOs and traditional PEOs operate under a co-employment model, providing small businesses with access to HR expertise and administrative support.

Through this arrangement, employers retain control of their workforce while the PEO helps manage critical HR functions.

Managing payroll and payroll taxes is complex and time-consuming for many small businesses. Both CPEOs and traditional PEOs streamline payroll operations by handling key administrative responsibilities, including:

However, not all payroll service providers offer the same level of protection. Here’s how different third-party arrangements compare:

Payroll Service Providers (PSPs)

Reporting Agents (RAs)

Section 3504 Agents

A CPEO offers unmatched protection by ensuring:

✔ Full IRS compliance and tax security.

✔ Clients retain their tax credits (which may be lost under a traditional PEO).

✔ Businesses avoid wage-base restarts and double payroll tax payments.

Choosing a CPEO vs PEO or payroll provider means fewer risks and greater financial peace of mind.

RELATED: The Surprising ROI of Payroll Outsourcing for Small Businesses >>

Employment regulations are constantly evolving, and failing to stay compliant can lead to costly penalties or legal disputes. Both CPEOs and traditional PEOs help businesses navigate complex compliance requirements, including:

✅ Payroll tax compliance – Ensuring accurate tax reporting and timely payments.

✅ Unemployment insurance – Managing state and federal UI requirements.

✅ Workers’ compensation – Providing proper coverage and claims management.

✅ Workplace safety – Assisting with OSHA compliance and risk mitigation.

✅ HR compliance – Keeping policies aligned with labor laws and industry regulations.

A strong benefits package helps small businesses attract and retain talented employees. Both CPEOs and traditional PEOs help employers access high-quality benefits at more competitive rates, including:

✅ Health, dental and vision insurance – Group plans with better pricing.

✅ Retirement plans – 401(k) and other savings options.

✅ Insurance premium discounts – Lower rates due to larger risk pools.

✅ Enrollment and claims management – Simplified administration for employers and employees.

By partnering with a CPEO or PEO, small businesses can offer Fortune 500-level benefits without the high costs or administrative burden typically associated with managing benefits in-house.

Workplace safety is essential, yet many small businesses lack the internal expertise to identify hidden risks that could lead to injuries or costly regulatory violations.

Both CPEOs and PEOs provide safety guidance and risk management support, including:

✅ Workplace safety audits – Identifying hazards and compliance gaps.

✅ OSHA compliance assistance – Preparing for and responding to inspections.

✅ Injury prevention strategies – Implementing cost-effective safety measures.

✅ Risk mitigation training – Educating employees on workplace safety best practices.

When considering a CPEO vs PEO, both help reduce liability, lower workers’ comp costs and ensure regulatory compliance.

RELATED: Risk Management Strategies - The Transformative PEO Approach >>

In today’s competitive labor market, small businesses must take a strategic approach to recruiting and retaining talent. Both CPEOs and PEOs provide support throughout the hiring and employee development process, including:

✅ Recruiting and job positioning – Helping businesses stand out to top candidates.

✅ Applicant screening and assessment – Ensuring the right fit for each role.

✅ Onboarding support – Streamlining the hiring process for a smooth transition.

✅ Workplace culture development – Enhancing employee engagement and retention.

By partnering with a CPEO or PEO, businesses gain expert guidance to build a skilled, motivated workforce.

Managing workers’ compensation can be complex, requiring businesses to navigate claims, compliance and insurance premiums. Both CPEOs and PEOs take on this responsibility by:

✅ Handling workers' comp coverage – Ensuring businesses have the right insurance.

✅ Managing claims and paperwork – Reducing administrative burden.

✅ Ensuring compliance – Keeping businesses aligned with state and federal regulations.

✅ Providing risk management support – Helping reduce workplace injuries and lower premiums.

Offering retirement benefits is an important way for small businesses to support employees’ long-term financial security while remaining competitive in the job market.

Both CPEOs and PEOs assist employers with:

✅ 401(k) and retirement savings plans – Helping businesses choose the best options.

✅ Employer contribution strategies – Structuring plans to maximize employee benefits.

✅ Plan administration and compliance – Handling enrollment, reporting and regulatory requirements.

A CPEO or PEO makes it easier for small businesses to offer competitive retirement benefits while staying compliant.

Axcet Makes Offering Retirement Benefits Easy: Learn About Our Small Business 401(k) Plans >>

Tracking employee performance helps businesses identify strengths, address skill gaps and improve productivity.

Both CPEOs and PEOs support employers with tools and guidance for:

✅ Employee review processes – Developing structured evaluations.

✅ Performance metrics and goal setting – Using data to enhance productivity.

✅ Reskilling and development strategies – Offering training to strengthen workforce skills

Many small businesses do not have the resources to maintain a full in-house HR department. As a result, business owners or managers often find themselves handling complex HR challenges on their own.

Both CPEOs and PEOs provide ongoing HR guidance and support, including:

✅ HR policy development – Ensuring businesses stay compliant.

✅ Employee relations support – Managing workplace concerns effectively.

✅ HR consulting and best practices – Providing expert solutions for day-to-day issues.

If you're weighing a CPEO vs PEO, both enable businesses to gain access to expert HR professionals without the cost of an internal team. While both models provide these core services, IRS certification introduces several key protections that distinguish a certified PEO from a traditional PEO.

RELATED: PEO Cost Considerations - Is It Worth the Investment? >>

Choosing a CPEO is a significant decision, and the right fit can impact your business's HR functions, compliance and growth. Before selecting a provider, ask these five key questions:

RELATED: Top Benefits of Hiring SHRM or HRCI Certified HR Consultants >>

RELATED: Level Funded vs Self Funded vs Fully Funded >>

✅ A thorough vetting process ensures you choose a CPEO that aligns with your business needs and goals.

Understanding the differences between a certified PEO vs non-certified PEO can help business owners make a more informed decision when choosing an HR partner.

Axcet HR Solutions has been a trusted PEO since 1988 and was among the first 10% of PEOs nationwide to achieve IRS certification as a CPEO in 2017.

We’ve maintained that certification uninterrupted, ensuring small and mid-sized businesses receive trusted, compliant and expert HR support.

✅ Recruiting and Onboarding Support

✅ Better Benefits at Competitive Rates

✅ Local, Personalized HR Expertise

✅ Unmatched Industry Experience

Want to Learn More? Download Our FREE eBook: Certified PEOs - Your Easy to Understand Guide >>

If you're weighing the benefits of a certified PEO vs. non-certified PEO, Axcet offers the peace of mind that comes with full IRS certification and decades of trusted experience.

📞 Contact us today to learn how partnering with an IRS-certified PEO can benefit your business.

* The IRS does not endorse any particular certified professional employer organization. For more information on CPEOs, go to www.irs.gov

Written by

Jo McClure, CPP, is the Director of Payroll Administration at Axcet HR Solutions, where she has been a pivotal leader for over 20 years. With more than two decades of experience in payroll outsourcing and professional employer organizations (PEOs), Jo specializes in helping small to mid-sized businesses navigate payroll administration, employee benefits, and compliance.

Her strategic leadership at Axcet focuses on implementing best practices in payroll management, compliance auditing, and risk mitigation. Jo obtained her Certified Payroll Professional (CPP) designation in 2006 and has held numerous leadership roles in the Greater Kansas City Chapter of the American Payroll Association, including President, Vice President, and Chapter Coordinator. A frequent speaker at the Midwest Regional Payroll Conference, she has also contributed articles to publications such as Thinking Bigger Business and Kansas City Small Business Monthly.

Jo’s expertise has been recognized through industry publications. She co-authored the article “High-Touch in the Age of High-Tech: How PEOs Can Embrace AI Without Losing Their Humanity” https://peoinsider.org/articles/high-touch-in-the-age-of-high-tech-how-peos-can-embrace-ai-without-losing-their-humanity/ for PEO Insider (March 2026), alongside Jeanette Coleman, SPHR, SHRM-SCP, and authored “PEOs in the Community: Axcet Making Philanthropy Part of the Company’s Culture” https://peoinsider.org/articles/peos-in-the-community-axcet-making-philanthropy-part-of-the-companys-culture/ (November 2025). These contributions reflect her perspective on balancing technology-driven payroll and HR processes with the human experience, as well as the role of community engagement in building strong organizational cultures.

Jo's specialties include payroll implementation, compliance auditing, and crafting best-practice payroll solutions that ensure businesses stay compliant while optimizing their processes.

Published in: PEO Insider

.webp)

Let us know what you think...