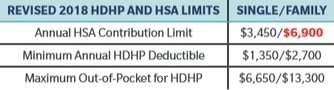

The IRS has announced it is modifying the annual limitation on deductions for contributions to a health savings account (“HSA”) allowed for taxpayers with family coverage under a high deductible health plan (“HDHP”) for the 2018 calendar year. Under Rev. Proc. 2018-27, taxpayers will be allowed to treat $6,900 as the annual limitation, rather than the $6,850 limitation announced in Rev. Proc. 2018-18 earlier this year.

The IRS has announced it is modifying the annual limitation on deductions for contributions to a health savings account (“HSA”) allowed for taxpayers with family coverage under a high deductible health plan (“HDHP”) for the 2018 calendar year. Under Rev. Proc. 2018-27, taxpayers will be allowed to treat $6,900 as the annual limitation, rather than the $6,850 limitation announced in Rev. Proc. 2018-18 earlier this year.

The HSA contribution limit for individuals with family HDHP plan coverage was originally issued as $6,900 last May in Rev. Proc. 2017-37. Earlier this year, the IRS announced a $50 reduction in the maximum deductible amount from $6,900 to $6,850 due to changes made by the Tax Cuts and Jobs Act.

Due to widespread complaints and comments from individual taxpayers, employers and other major stakeholders, the IRS has decided it is in the best interest of “sound and efficient” tax administration to allow individuals to treat the originally released $6,900 as the 2018 family limit. The IRS acknowledged many individuals had already made the maximum HSA contribution for 2018 before the deduction limitation was lowered and many other individuals had made annual salary reduction elections for HSA contributions through employers’ cafeteria plans based on the higher limit. Additionally, the costs of modifying various systems to reflect the reduced maximum would be significantly greater than any tax benefit associated with an unreduced HSA contribution.

Alternatively, if an individual decides not to repay such a distribution it will not have to be included in gross income or subject to the additional 20 percent tax as long as the distribution is received by the individual’s 2018 tax return filing due date. This tax treatment, however, does not apply to contributions from an HSA that are attributable to employer contributions if the employer does not include any portion of the contributions in the employee’s wages because the employer treats $6,900 as the annual contribution limit. In that scenario, the distribution would be included in the individual’s gross income and subject to the 20 percent additional tax unless it was used to pay for qualified medical expenses. In other words, if the employee withdraws the $50 and does not return it to the HSA, it’s not includible in income or subject to the 20 percent additional tax unless the $50 is reported as an employer contribution on the employee’s W-2 (in box 12, code W), in which case it would be includible in income and subject to the 20 percent additional tax.

Employers who previously informed employees the limit was lowered should consider informing them now about the new limit and repayment option.

For the second time this year, anyone processing payroll will need to adjust all HSA contributions for ALL employees due to a minimal $50 per year contribution limit change by the IRS. Not only is this an inconvenience, but it is also creates an opportunity for payroll mistakes. In fact, 33 percent of small businesses are fined by the IRS each year for payroll errors.

Download our FREE report now and find out five reasons you do not want to process payroll.

Written by

Jo McClure, CPP, is the Director of Payroll Administration at Axcet HR Solutions, where she has been a pivotal leader for over 20 years. With more than two decades of experience in payroll outsourcing and professional employer organizations (PEOs), Jo specializes in helping small to mid-sized businesses navigate payroll administration, employee benefits, and compliance.

Her strategic leadership at Axcet focuses on implementing best practices in payroll management, compliance auditing, and risk mitigation. Jo obtained her Certified Payroll Professional (CPP) designation in 2006 and has held numerous leadership roles in the Greater Kansas City Chapter of the American Payroll Association, including President, Vice President, and Chapter Coordinator. A frequent speaker at the Midwest Regional Payroll Conference, she has also contributed articles to publications such as Thinking Bigger Business and Kansas City Small Business Monthly.

Jo’s expertise has been recognized through industry publications. She co-authored the article “High-Touch in the Age of High-Tech: How PEOs Can Embrace AI Without Losing Their Humanity” https://peoinsider.org/articles/high-touch-in-the-age-of-high-tech-how-peos-can-embrace-ai-without-losing-their-humanity/ for PEO Insider (March 2026), alongside Jeanette Coleman, SPHR, SHRM-SCP, and authored “PEOs in the Community: Axcet Making Philanthropy Part of the Company’s Culture” https://peoinsider.org/articles/peos-in-the-community-axcet-making-philanthropy-part-of-the-companys-culture/ (November 2025). These contributions reflect her perspective on balancing technology-driven payroll and HR processes with the human experience, as well as the role of community engagement in building strong organizational cultures.

Jo's specialties include payroll implementation, compliance auditing, and crafting best-practice payroll solutions that ensure businesses stay compliant while optimizing their processes.

Published in: PEO Insider

.webp)

Let us know what you think...